Electrification is one of the most transformative and irreversible trends in the forklift market, writes Maya Xiao, Research Manager at Interact Analysis. The systemic shift from internal combustion engines (ICE) to electric powertrains, predominantly lithium-ion (Li-ion) batteries, is fundamentally reshaping the industry’s competitive dynamics, operational protocols, and environmental impact.

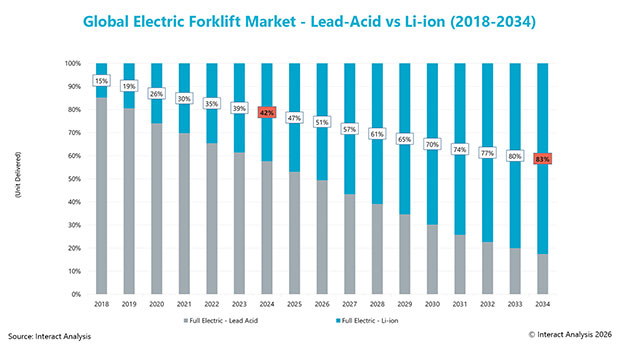

Our recently published Forklifts – 2025 report charts the meteoric rise of Li-ion forklifts and projects penetration rates will soar from approximately 32% in 2024 to over 70% by 2034 within the full-electric sector (which includes Li-ion and Lead-Acid models). A pivotal industry inflection point is expected around 2026, when Li-ion technology is forecast to surpass lead-acid batteries in market share within the electric forklift segment.

By 2034, a staggering 83% of all new electric forklifts shipped globally will be powered by Li-ion batteries. This rapid transition is overwhelmingly driven by the compelling operational and economic advantages of Li-ion technology.

The trajectory of electrification varies widely across geographical regions, reflecting differing economic structures, regulatory pressures, and market maturity.

China is the primary engine of global Li-ion penetration. Its Li-ion forklift shipments are projected to explode from 26,436 units in 2018 to over 1 million units annually by 2034.

Europe is advancing rapidly, driven by stringent emissions standards and strong corporate ESG mandates.

North America lags significantly behind, with the US not expected to reach 50% Li-ion penetration until 2032.

Despite the clear growth trajectory for electrified forklifts, the transition from ICE and lead-acid machines faces significant headwinds, such as:

High upfront capital outlay: The initial investment for Li-ion forklifts and the requisite charging infrastructure remains a primary barrier, especially for budget-conscious SMEs.

Complex infrastructure requirements: The most critical customer friction point is electrical infrastructure. Data indicates 50-60% of charging installations require facility upgrades, which can add up to 25% to the total project cost.

Supply chain and expertise gaps: While improving, the supply chain and after-sales market for Li-ion components are not yet as mature as those for ICE or lead-acid technologies.

Forklift electrification has passed the tipping point, evolving from a forward-looking trend into a core strategy that determines future enterprise competitiveness. Proactive leaders who actively adopt electrification are leveraging significant operational cost advantages, enhanced sustainability credentials, and superior supply chain resilience. In contrast, enterprises that lag behind may face the dual pressures of cost disadvantages and technological misalignment. As battery technology continues to advance, lifecycle cost advantages increase, and charging infrastructure becomes more refined, electric forklifts are rapidly transitioning from a “preferred option” to the “default configuration” in global industrial and logistics sectors, redefining the future landscape of material handling.

Comments are closed.