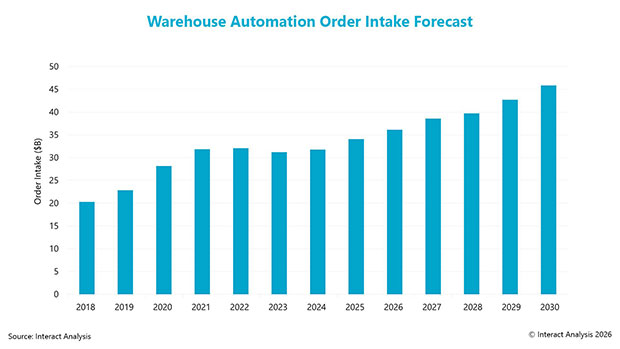

2025 was a tale of two halves for warehouse automation. At the beginning of the year, conditions appeared positive, with interest rates expected to fall and vendors reporting stronger pipeline activity. However, early in 2025, tariffs announced by US President Donald Trump introduced a sharp rise in uncertainty. As a result, many companies reported the postponement of large capital expenditure projects. Toward the end of the year, however, uncertainty declined more quickly than anticipated, and order intake for 2025 ultimately grew by 7%, exceeding our previous expectations.

Higher order intake was driven primarily by two key factors. First, higher steel costs resulting from 25% US steel and aluminium tariffs led to higher system prices, which pushed up order intake from a nominal dollar perspective. Second, a small number of end-customers made significant investments which, collectively, were large enough to move the needle and support market growth.

As a result of selected end-customers making outsized investments in 2025, we saw a corresponding concentration of growth among a limited number of automation vendors. This small number of vendors achieved significant growth, while the majority, particularly those focused on small to mid-sized customers, performed less well.

For example, Dematic’s order intake grew by 50% in the first three quarters, while Toyota Industries’ Logistics Systems order intake grew by 65% over the same period. TGW also reported strong performance, with order intake rising by 55% in its 2025 financial year (ending October).

While these large automation vendors performed particularly well, this positive sentiment was not shared across the wider market. Most automation vendors experienced sluggish performance in 2025.

What’s causing this performance disparity?

This divergence in performance between vendors is largely driven by two factors: first, the size of the vendors and their ability to service large-scale projects, and second, the strength of their existing relationships with the end-customers making these large investments. Small and medium enterprises (SMEs) slowed down CapEx spending in 2025 owing to the uncertainty caused by the tariffs. However, we saw a small number of large end-customers make extremely large investments in warehouse automation.

This marks a shift from the previous few years, during which automation vendors focused on small to mid-sized end-customers typically outperformed those targeting large accounts. In the years following the pandemic, large end-customers slowed their investment activity after overbuilding during the Covid-19 pandemic, while SMEs continued to invest at disproportionately higher levels. In contrast, in the current geopolitical environment, SMEs have become more cautious and have therefore slowed their investments.

Bucking the trend

Several mobile robot vendors significantly outperformed the wider market. Geek+, for example, reported 30% growth in order intake in the first half of the year. Meanwhile, a number of other mobile robot vendors also reported strong order intake following a more subdued 2024. Performance across the segment was uneven and not all mobile robot vendors performed well in 2025.

Final thoughts

In summary, 2025 was characterised by a small number of outsized investments that collectively moved the market. This enabled a limited number of large automation vendors to significantly outperform their competitors. We expect order intake to become more broad-based in 2026, with a growing share of investment likely to come from small and medium-sized end-customers as geopolitical and economic uncertainty continues to ease.

This trend will be further supported by increasing greenfield activity toward the end of 2026, as vacancy rates are projected to continue declining and the excess warehousing capacity built during the pandemic becomes more fully utilised.

Comments are closed.